- 10 Lenders Said No. SmartLend Found the One Who Said Yes — in 3 Days.

- Singapore SME Grants 2023–2026: What Actually Changed (And What Nobody Tells You)

- Why SME Loan Approval Rates Dropped to 70% — And What the Iran War Means for 2026

- Real CBS Makeovers: 3 Case Studies of SME Owners Who Turned Bad Credit Around

- Ask SmartLend: Why Did My SME Loan Get Rejected?

- Introducing SmartLend Concierge: A Helping Hand for SME Loans

- Legal Ways to Lighten Your Company’s Tax Burden in Singapore

- A Wake-Up Call on Director Duties: The Envy Saga and Other Cautionary Tales in Singapore

- Surviving Cash Flow Crunch: How SMEs Can Use Short-Term Financing Wisely

- Unmasking Business Loan Fraud: How Syndicates and Rogue Brokers Game Singapore’s Lending System—and How AI Can Stop Them

Estate Planning for Business Owners: What is Credit Protection Planning and Why is It Important

Every business plans to succeed, not to fail.

Having an estate plan is among the most important things in business planning, nevertheless it is a task many of us dread and put off dealing with until later in life, or sometimes just too late. While it may be “easy” to come up with a business strategy when unexpected challenges arise during your entrepreneur journey (when you are alive), estate planning is important as it deals with what happens after death, and when you are no longer around to make decisions.

The topic of after-death arrangements still remains a taboo subject especially in Asian culture. But as a business owner, after working so hard to build a successful business, deciding who will take over your business is a big decision and it should be an important part of business planning.

Many business owners are not aware of the importance of estate planning, or are simply overwhelmed by the concept of it. But don’t let that deter you.

What is Estate Planning?

Estate planning is the preparation of transferring and managing an individual’s assets in the unfortunate event of their incapacitation or death.

It is not just for the rich and famous.

In the case of business estate planning, it helps to ensure that your business matters are handled according to your wishes when you pass on or become disabled. Good planning helps to protect the business you have worked so hard for, especially when you want to pass down to the next generation smoothly.

Some aspects of business estate planning include business succession planning, credit protection, and having a buy-sell agreement in place.

If you have other business partners, think about when was the last time you talked to them about what happens should unexpected circumstances occur to one of you? Are they paying your family the market value of your company or your initial capital for your shares? Are they going to allow your family members to come onboard, taking your place, or has it ever been a topic of discussion at all?

If you are the sole business owner, that doesn’t make things any easier too. What would happen to your business if you weren’t around, will your family know what to do to take over the business, and are they prepared to pay off the outstanding business debts using their personal assets?

Thoughtful planning helps to minimize unnecessary legal costs involved in lengthy probate and it eliminates the emotional and financial stress that your family might have to face regarding your business matters when you are gone.

How Does Business Estate Planning Help?

The current Covid-19 pandemic has caused major disruptions to businesses, and over the past few months, we have seen a surge in the number of business loan applications. More than S$7.1 billion business loans have been disbursed over the past few months due to the coronavirus pandemic.

However, as simple as it seems, taking on a business loan and repaying it might not be so straightforward in the unfortunate event of a death or incapacitation. The implications it has on the remaining business partner(s), if any, and your family members can be very daunting.

Be it you are a new startup seeking financing, or an established business looking for a business loan for expansion, the problem with the loan repayment does not disappear when you are no longer around.

To understand how estate planning is important for businesses when there are outstanding business loans and debts, let us look at the following scenario, based on a true story of a business owner who did not do proper estate planning before his death.

Background of The Business Owner

Ah Wee had run a car polishing business and had been in this trade since young for more than 20 years. He started the business as a sole proprietor as it is the cheapest and easiest way to set up a company, in his opinion.

After many years in the business, his company grew and he began to hire a few staff. Converting the business into a “Private Limited” company had always been on his mind, but he was too busy and felt that it was too troublesome to do it. There was always something else more important that he had to do.

Ah Wee’s wife was previously in the oil and gas industry as a researcher, however her company restructured during the last financial crisis and she had lost her job since. She had been a stay home mom for the past ten years taking care of their young children.

Over the years, Ah Wee’s business did well, however his workshop only allowed him to polish two cars at any one time. To expand his business further, Ah Wee took up a business loan and moved out to a bigger premise so that he could have space to accommodate more cars.

One day, Ah Wee experienced difficulties in breathing and chest discomfort while at work. He informed his staff that he was going to see a doctor and might go back home to rest. Unfortunately, that evening, his wife found him motionless in bed.

Problems That Arise After His Demise

Ah Wee’s wife had never been involved in the business. With his demise, nobody knew what to do and his staff began to leave as they did not know if the business would carry on.

Suppliers also came knocking at the door to demand for payment upon hearing Ah Wee’s demise.

Ah Wee’s wife was faced with immense stress. She had just received a letter of demand from the bank claiming from the estate of her late husband, as he had acted as a personal guarantor for the business loan that he had taken for the business expansion.

At a loss of what to do after losing her loved one and the sole breadwinner of the family, not only was she faced with the possibility of selling the house, she also had no idea how she was going to support her young children.

The above scenario happens in real life. Very often, business owners have the tendency to put off estate planning as there is always something else more important to do, something else that is more urgent - such as focusing and growing their business. Or they just simply have the “It wouldn't happen to me” attitude.

Why is Estate Planning Important?

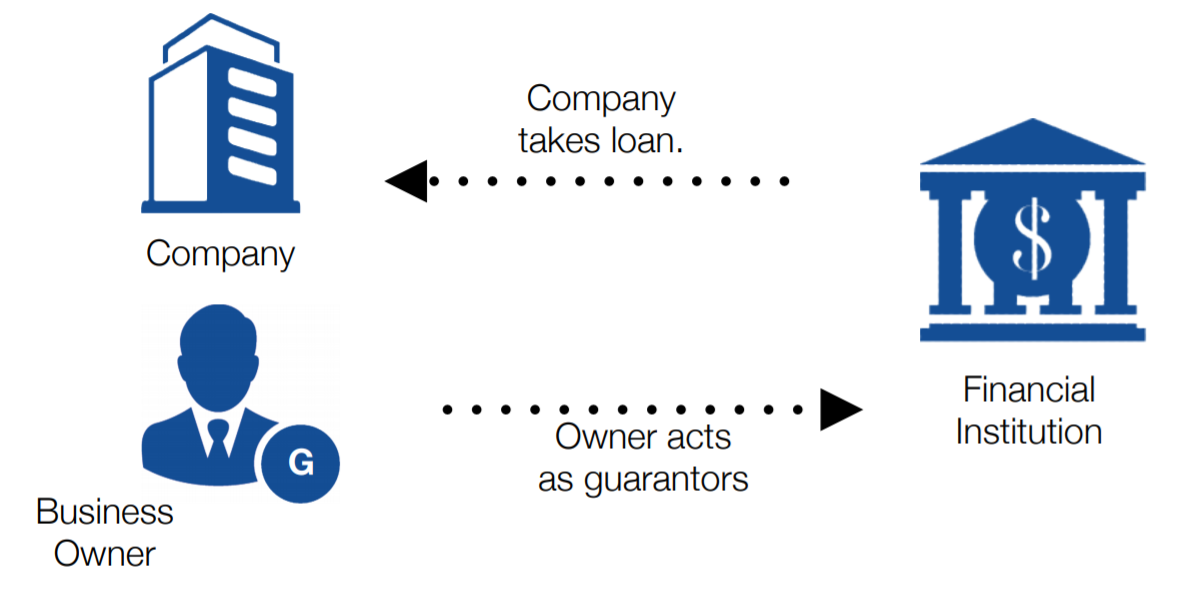

Many businesses take up credit facilities for their working capital or business expansion. Most companies started up with capital funds contributed by the business owner(s) and subsequently operate from retained profits of the company. These funds are limited hence most companies may turn to external sources such as a financial institution for credit facilities, like a business bank loan, in order to expand their business.

Financial institutions always require a Personal Guarantee, that is, the business owner(s) or partners to act as guarantor(s) for the loan. This means that, all parties are liable for 100% of the loan amount in the event the company and the partners / directors default on the business loan.

What most people are not aware is:

- Death does not release your responsibility as a guarantor. Financial institutions can seek to recover debts from the surviving guarantor(s) and the estate of the deceased guarantor if the company does not have sufficient funds to pay off the outstanding loan.

- When a director acts as a guarantor for a company, this duty does not discharge automatically even when you leave your director role. Most financial institutions have a legal clause that covers current and future company loans.

Being a company director / partner and acting as a guarantor for a business loan can have catastrophic effects on your family. Without proper estate planning, your family members can be put into unnecessary emotional and financial stress.

Statistics have also shown that many businesses collapse when the business owner or key decision maker passes on.

No business owner plans to fail, however, like in Ah Wee’s case, they just fail to plan.

Credit Protection Planning As a Solution

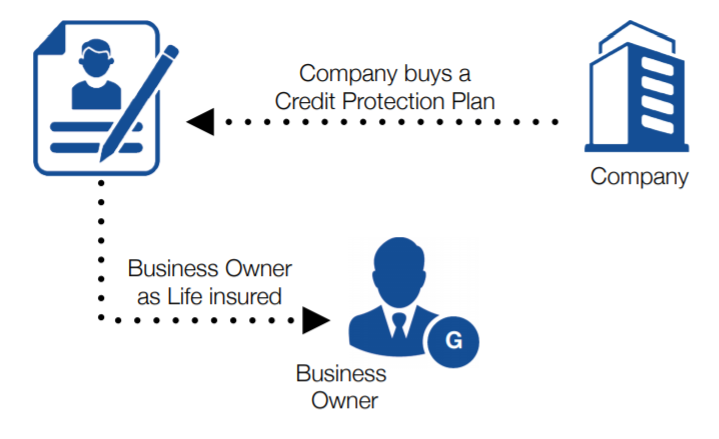

Proper estate planning for businesses also involves Credit Protection Planning. This will help to discharge the responsibility of the guarantor in the event of his or her death.

Other benefits include:

- Settlement of any outstanding business debts and loans, giving the company a positive bank balance for the successor to take over operations smoothly.

- Allow the company to continue to operate should financial institutions decide to withdraw all credit facilities in event of the demise of the guarantor.

When a company takes up a business loan:

Company can take up a Credit Protection Plan for the business owner:

In the event that the business owner passes on or becomes total and permanently disabled,

Company is now debt free and business operation is uninterrupted, thus allowing the successor or remaining partners to continue with the business.

With a Credit Protection Plan in place, it allows the company to better position itself financially to continue its operation. It also gives the living director(s) / partners a peace of mind knowing that as a guarantor, his role will be discharged and his personal estate is protected in the event of incapacitation or death.

If Ah Wee had done proper estate planning and had a Credit Protection Plan in place, his wife would not need to sell the house to clear the outstanding business debts and loans.

He could even have created an opportunity for his wife to learn the ropes and take over his business, so that her children and her daily living needs will also be well taken care of.

At Smart Towkay, we believe that business owners should be well-informed not just in making the right business decisions when it comes to a business expansion, taking up a business loan, or being aware of the various Government support and grants that are available, but business owners should also be prepared to plan for what happens when they are no longer around, should unforeseen circumstances occur.

Every business will face unique challenges and require different solutions.

Contact us to find out more about how Credit Protection Planning could help in protecting your business, especially if your company has just been approved of a business loan.

Remember to bookmark this page as we will have a series of articles on estate planning for business owners! If you have a specific scenerio that you would like to discuss, do share it with us!

About the author: Joshua Lee, an Estate Planner and Chartered Financial Consultant, with 15 years of experience in advising business owners in risk management.

-------------------------------------------------------------------------------------------------------

Not sure whether your company can be qualified for bank loans or alternative lending? Try our A.I assisted loan, and Smart Towkay team will send you a lending report within 24 hours' time. With the lending report, we aggregate and recommend the highest chance of approval be it with BANKS / FINANCIAL INSTITUTIONS or Alternative lenders like Peer to Peer Lenders or even B2B lender!

Got a Question?

WhatsApp Us, Our Friendly Team will get back to you asap :)

Share with us your thoughts by leaving a comment below!

Stay updated with the latest business news and help one another become Smarter Towkays. Subscribe to our Newsletter now!