- 10 Lenders Said No. SmartLend Found the One Who Said Yes — in 3 Days.

- Singapore SME Grants 2023–2026: What Actually Changed (And What Nobody Tells You)

- Why SME Loan Approval Rates Dropped to 70% — And What the Iran War Means for 2026

- Real CBS Makeovers: 3 Case Studies of SME Owners Who Turned Bad Credit Around

- Ask SmartLend: Why Did My SME Loan Get Rejected?

- Introducing SmartLend Concierge: A Helping Hand for SME Loans

- Legal Ways to Lighten Your Company’s Tax Burden in Singapore

- A Wake-Up Call on Director Duties: The Envy Saga and Other Cautionary Tales in Singapore

- Surviving Cash Flow Crunch: How SMEs Can Use Short-Term Financing Wisely

- Unmasking Business Loan Fraud: How Syndicates and Rogue Brokers Game Singapore’s Lending System—and How AI Can Stop Them

Best SME Business Loan Comparison in Singapore 2020

.jpg)

As a Small and Medium-sized Enterprise (SME) ourselves, and dealing with many SME owners over the years, we at Smart Towkay understand the pain points of SMEs when it comes to applying for an SME business loan in Singapore.

This year 2020 will definitely be a memorable year for all SME owners in Singapore. The Covid-19 pandemic and recession have disrupted many businesses and affected cash flow especially during the Circuit Breaker period. This is where an SME loans in Singapore is able to help SMEs tide through this difficult time, and provide the cash flow that is more important than before.

Why Do You Need an SME Business Loan?

The issue of cash flow continues to haunt SMEs be it you are a new startup, or many years into the business. It may not necessarily mean that your business is not doing well, but sometimes business opportunities may require a sum of money to be invested first. You want to ensure that your business has a healthy cash flow and be prepared for any business opportunity that can come unexpectedly.

Common reasons to get an SME business loan includes:

- To purchase inventory and machinery / equipment

- To finance daily operations costs

- To expand your business

- To improve and expand marketing strategies

- To fund a new business opportunity with higher ROI (returns on investment)

What is an SME Business Loan?

An SME loan is, as its term denotes, a sum of money that SMEs borrow to use for business related purposes. It is usually over a period of time where SMEs repay the principal amount with interest. Repayment period usually stretches up to 5 years.

SME business loans in Singapore are typically provided by banks and other financial institutions (FIs).

If you are reading this article, it is likely that you are looking for an SME business loan for your company. To know which business loan is suitable for you, it is perhaps good for you to familiarize yourself with the different types of business loans that are available - unsecured business loans, working capital loans, micro loans, temporary bridging loans, machinery and equipment loans, asset-backed financing products, factoring etc.

Each bank and fin140ancial institution also offers different types of SME business loans, with different interest rates and criteria to qualify.

Nevertheless, if you do not want to go through the hassle of reading up on the different types of SME business loans available, you can simply click here for a free loan assessment and we will guide you through!

Types of SME Business Loans in Singapore

| Type of Loan | Maximum Loan | Loan Tenure | Interest Rate |

Unsecured Business Term Loan

|

S$500,000 | 1-5 years | 5-11% p.a |

Enhanced SME Working Capital Loan

|

S$1 million | Up to 5 years | 2-5% Capped at 5% p.a.. |

Temporary Bridging Loan Programme*

|

S$5 million | Up to 5 years | 2-5% capped at 5% p.a. |

Asset-backed Financing

|

Up to 90% equipment value | Up to 5 years | 1.4-2.5% |

Equipment Financing

|

Up to 90% equipment value | Up to 5 years | 1.8%- 2.5% p.a. |

Trade Financing

Factoring / Receivables Financing

|

Up to 90% Invoice value | 90 - 120 days | 2-4% |

Peer To Peer (P2P) / Business To Business (B2B) Funding

|

Up to $1 Million | 1 - 24 months | P2P: 1-3% per month B2B:3-7% per month |

*The Temporary Bridging Loan Programme is a government assisted financing scheme introduced in Budget 2020. This scheme is now eligible to all sectors after the Solidarity Budget Enhancement.

Repayment period is capped at 5 years.

|

The participating financial institutions are as below: |

|

CIMB Bank Berhad |

|

DBS Bank Ltd |

|

Ethoz Capital Ltd |

|

Hong Kong and Shanghai Banking Corporation |

|

Hong Leong Finance Ltd |

|

IFS Capital Ltd |

|

Maybank Singapore Ltd |

|

ORIX Leasing Si140ngapore Ltd |

|

Oversea-Chinese Banking Corporation Ltd (OCBC Bank) |

|

Resona Merchant Bank Asia Ltd |

|

RHB Bank Berhad |

|

Sing Investments & Finance Ltd |

|

Singapura Finance Ltd |

|

Standard Chartered Bank |

|

United Overseas Bank Ltd |

What are the Qualifying Criteria for a Business Loan In Singapore?

The very basic requirement for an SME to apply for a business loan in Singapore is that the company must be locally registered with at least 30% local shareholding.

As lending criteria differ across different banks and FIs, there are many other factors and conditions that will affect a company’s eligibility to qualify for a business loan. As a business owner, you need to take note of the following 3 key factors that will affect your business loan eligibility :

Duration of business operations in Singapore

The longer a company has been in operation, the more stable the business is. Most banks and FIs deem a company as reasonably stable when it has been in operations for at least 2 years.

For new startups, banks such as DBS and OCBC have a lenient incorporation criteria, thus new startups can approach them for their first business loan.

Annual turnover of company

Banks generally prefer companies that show an annual turnover of S$300,000 and above. This is also used as a gauge to determine the loan amount that your company qualifies for.

Credit Bureau Score

Lenders look at your credit report to determine your company’s loan quantum, as well as your personal credit history to determine the chances or capability of your repayment of the loan.

For credit bureau rating that are not so ideal, do look out for alternative funders such as Peer to Peer or Business to Business lenders as usually their loan tenure are much shorter, thus some will overlook bad credit rating and their lending analysis will be more on the SME’s short term cash flow ability such as ad-hoc factoring of soon-to-be realized invoices.

How to Apply for an SME Business Loan?

The required documents may vary across different banks and FIs, however the general documents that every lender will need to process your application are:

- Past 6 months bank account statements

- Profit and Loss statements

- Balance sheet

- Income tax returns of Directors for past 2 years

- NRIC of Directors

Applying for an SME business loan can be a long and tedious process due to stringent requirements of banks and FIs in Singapore. Having all the required documents ready will help to speed up the application process. The most important part is to convince the lender that your business is strong and stable to take on a business loan, and have the capability to repay it. Moreover, the last thing you want is to default on the business loan.

Again, if you do not wish to go through the hassle of liaising with different banks, you can simply click here for a free loan assessment and we will guide you through!

Read also: Do You Really Need A Loan Broker?

Terminology:

These are the terms commonly sighted in your bank offer letter

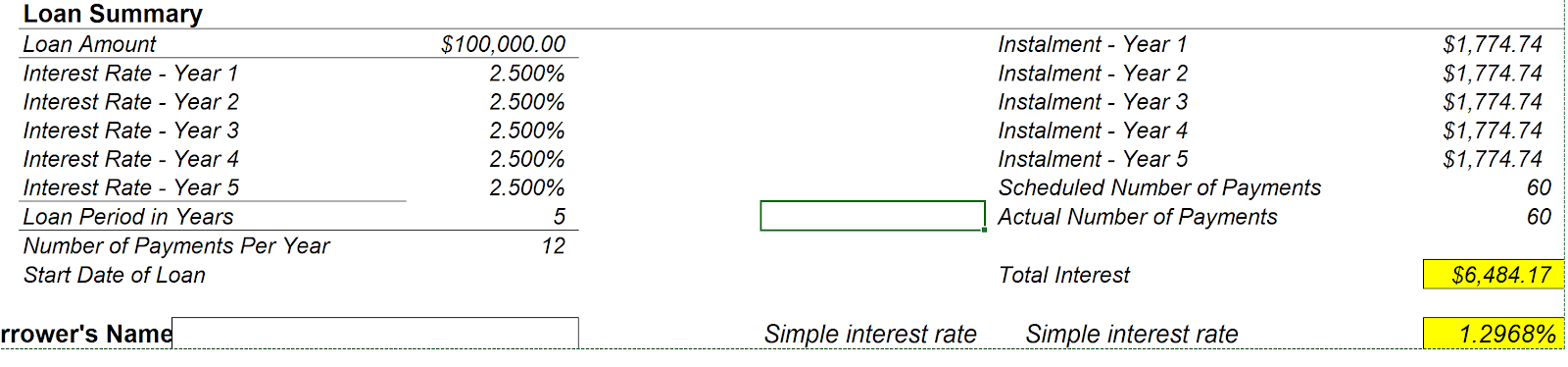

1. Effective Interest Rates:

Effective interest rate is the true cost of a loan, over a given period, on a reducing balance basis.

Often, SME owners confuse the E.I.R as the actual cost of financing i.e $100,000 loan at 2.5% effective interest rate does not equate to 2.5% x $100,000 = $2,500 interest payable per year.

As it is on a reducing balance basis, the average simple rates per annum should be at 1.2968% or $1,296.80 payable per annum for a $100,000 loan.

Effective interest rates are rates commonly quoted by financial institutions

2. Simple Interest Rate:

This is like your car loan calculation and commonly used by Peer To Peer or Business To Business Lenders.

E.g $100,000 loan at 12% per annum = $12,000 interest payable per year.

3. Lock-In Period:

Unless SMEs take up banks’ in-house loans, under the Government-assisted Enterprise Singapore Financing Scheme, loans will not be subjected to any full or partial redemption penalty.

This means that SMEs can repay their Temporary Bridging Loan or Enhanced Working Capital Loan anytime during their repayment period without incurring any redemption penalty, and they just have to serve one month notice period.

-------------------------------------------------------------------------------------------------------

Got a Question?

WhatsApp Us, Our Friendly Team will get back to you asap :)

Share with us your thoughts by leaving a comment below!

.png)

.png)