- 10 Lenders Said No. SmartLend Found the One Who Said Yes — in 3 Days.

- Singapore SME Grants 2023–2026: What Actually Changed (And What Nobody Tells You)

- Why SME Loan Approval Rates Dropped to 70% — And What the Iran War Means for 2026

- Real CBS Makeovers: 3 Case Studies of SME Owners Who Turned Bad Credit Around

- Ask SmartLend: Why Did My SME Loan Get Rejected?

- Introducing SmartLend Concierge: A Helping Hand for SME Loans

- Legal Ways to Lighten Your Company’s Tax Burden in Singapore

- A Wake-Up Call on Director Duties: The Envy Saga and Other Cautionary Tales in Singapore

- Surviving Cash Flow Crunch: How SMEs Can Use Short-Term Financing Wisely

- Unmasking Business Loan Fraud: How Syndicates and Rogue Brokers Game Singapore’s Lending System—and How AI Can Stop Them

INVESTING 101: Does Investing In Your Own Co-Living Space Live Up To The Hype?

So co-working spaces like WeWork and JustCo are pretty ubiquitous by now, but have you heard of co-living spaces?

With the rise of the sharing economy, co-living developments offer private apartments with communal facilities such as lounge and relaxation areas. These are mainly catered to young professionals.

This is especially ideal in land-scarce Singapore, where rental prices are through the roof and paying for a space with shared facilities instead of renting the whole apartment can significantly reduce rental outlay.

In Singapore, the big institutional players are Hmlet, Ascott, and Figment, just to name a few.

In this article, we are not talking about co-living spaces which are operated by institutions. Instead, the focus will be on ‘’D.I.Y” co-living spaces investment that are operated by individuals.

How Does It Work?

A few ‘property gurus’ have been conducting seminars recently, preaching the concept of being an individual co-living operator and claiming to be the “First in Asia” to have come up with this concept. (Apparently, investing in industrial properties with no stamp-duty fee, and partitioning it to rent out to multiple tenants, is no longer sexy.)

These “gurus” teach their students to rent a private apartment, refurbish it, and then rent out individual rooms to separate tenants. Essentially, one is subletting a 3 bedder condominium to 3 individual tenants and all share the same communal areas. This is hardly revolutionary, surely. In fact, this is pretty much how room rentals work since the concept of sub-letting came into existence.

Nevertheless, innovative or not, this is still quite an attractive concept isn’t it?

The advantages that have been bandied about are:

1. No huge capital outlay required

Compared to investing in industrial property for rental purposes, the outlay for this co-living concept will be only S$15,000-S$20,000 per co-living space. This cost includes 2 months rental deposit, renovation costs of not more than S$5,000, and monthly miscellaneous costs like WiFi and utilities.

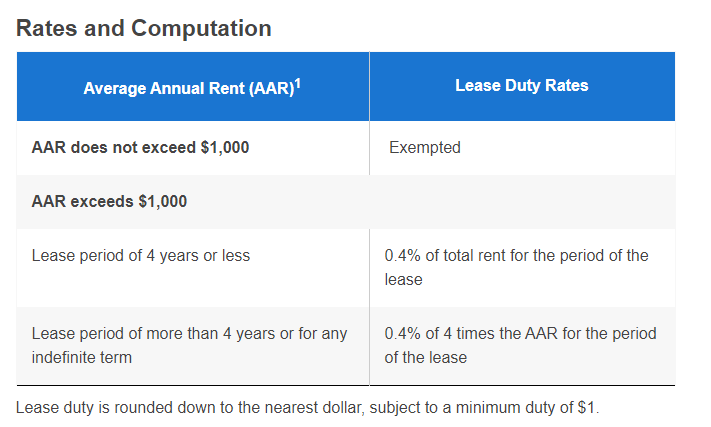

2. No Stamp Duty

This is what they are preaching that compared to buying industrial/commercial properties, there are no stamp duty involved in this investment. Really? Stamp duty is still payable on the contractual rental on the market rental, whichever is higher at the lease duty rates.

Source: IRAS Tax Portal

3. ROI of 300%

This is the interesting part. Say you rent a 3 bedder apartment at a good location for S$4,000 per month. The “guru” would advise you to commit to a 3-year lease at least to maximise your returns, especially since capital is thrown in to refurbish the apartment.

The going rate per room in these good locations would probably be approximately S$1,500. Spend a good S$5,000 to spruce up the place (i.e a fresh coat of paint, buying some fancy new furniture etc). This way, when the rental is listed on the various property platforms, your apartment will stand out and you can rent it out perhaps at a higher price of S$1,800. Thus S$1,800 x 3 = S$5,400. Profit of S$1,400 per unit! And why stop at one? Let’s rent another 10 units and this becomes passive income of S$14,000 per month.

4. Face no legal barriers to growth

The Singapore government tends to step in with legislation to regulate the purchase of residential and industrial properties when the market heats up. However, rental and sublease markets are, by and large, undisturbed.

Other property investment options often require one to pool resources with other investors to purchase an industrial/commercial unit (the concept of minimum or no downpayment scheme) and perhaps even get a loan. In comparison, this co-living concept seems to be both a safer and less troublesome option.

What Can Go Wrong With This Investment?

1. Is This Really “Co-Living” And Can You Charge Like One?

First of all, we should remove the rose-tinted glasses which are placed on our noses during these co-living investment seminars, and look at this concept for what it is.

Ultimately, the term “co-living” is used loosely here as this is merely operating rental apartments. One does not actually offer the community elements that characterise genuine co-living operators. If one does, the costs would rise accordingly, and to untenable heights.

Co-living institutions offer shared spaces such as gyms and movie screening rooms as well as shared services such as cleaning and laundry. In addition operators expend resources to build a community amongst its residents by organising social events, workshops and gatherings etc. Many of them even have a rudimentary screening process to try and match the right group of tenants living together in a co-living space.

These aren’t just perks; they are the essences of what defines the co-living concept and justifies the price for those who are looking for such an experience. In the absence of these features, would just a fancy looking room really command such a high rental fee to make up the attractive ROI?

In addition, the ROI does not factor in agent fees/stamp duty fees, which usually constitute half to one month’s rental fee per year lease.

2. Singapore Market

Co-living is a big thing in the US and Europe, and institutional operators are raising huge investment funds to operate in this asset class.

This is due to the target audience, which are the younger generations that typically cannot afford to purchase their own properties but would pay a premium for the convenience of flexible lease terms, furnished units, housekeeping, fitness centres and co-working space, all in one place for one price.

But in Singapore, a recent survey by the National Youth Council shows 97% of unmarried individuals still stay with their parents.

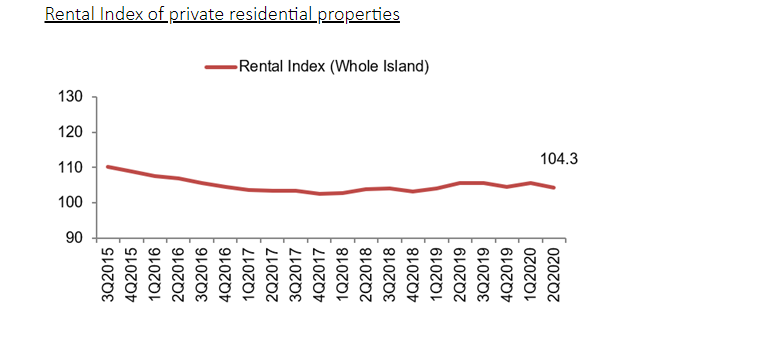

In the recent rental market price index report by URA, rental prices have gone down by 1.2% in the 2nd quarter of 2020. With rental prices going down, and a small percentage of locals renting, the target market doesn’t seem to be very big.

3. Expatriates / Foreigners In Current Covid-19 Situation

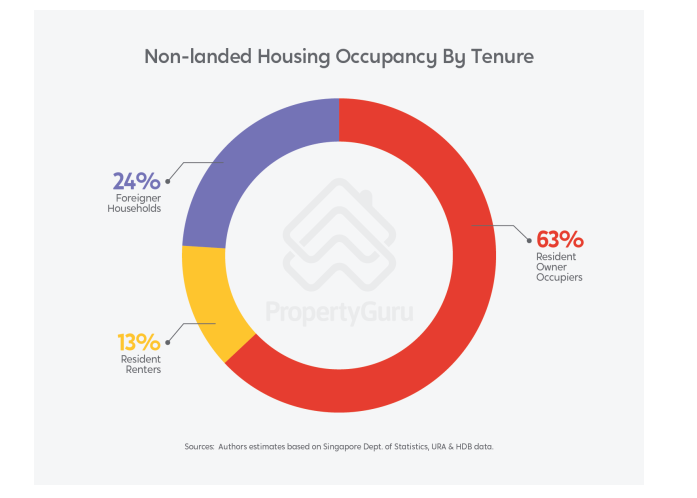

According to Property Guru, foreigners make up about 24% of non-landed properties occupancy and about 65% of all rental properties in Singapore.

Next, let’s eliminate foreigners that are on work permits and foreign domestic workers who do not need to rent. Based on MOM statistics in June 2020, the number of eligible foreigners are 747,500. Moreover, given the current Covid-19 situation and with all the hiring incentive to hire locals, the expatriate market is expected to shrink by another 200,000 by end of this year.

With the rental market shrinking to a transaction volume of 2,881 in May 2020, the investors are fighting with other direct landlords, serviced apartments and institutional co-living operators for the same pool of tenants.

The ROI calculated by these “gurus” is based on full occupancy with a minimal lull period but any apartment that remains vacant for more than 2-3 months will result in serious cash flow problems for the investors although they claimed that most of their students manage to get full occupancy within 2-3 weeks of committing to the lease and if the scheme really works, is a matter of time property agents will advise their landlords to do the same thus cutting the supply.

Conclusion

At the end of these seminars, as per all other investment seminars there are the course fees needed to be paid for their ‘masterclass’. In this case, the price is about S$2,000+.

To be fair, it includes more in-depth explanations of the scheme as well as the tools to assist in this investment such as sub-tenancy agreement templates, and teaching how to negotiate with landlords for a cheaper rental due to longer lease commitment. It also assists help to find cheap renovation firms and furniture for the refurbishment and helps in building a community where students can cross-refer tenants to each other’s rental units.

We wouldn’t deny that this scheme will attract even the most savvy investors as the upsides could potentially outweigh the initial capital outlay. Assuming a rosy environment post-covid, this scheme might actually work with the influx of expatriates flooding back into the rental market.

Of course, with all investment schemes - even MLM schemes, there are bound to be individuals that make money out of it and give rave testimonials. But our advice? Don't get FOMO. Think twice before putting your hard earned money into this investment given the current gloomy outlook on the rental market.

Read also: Top 2020 “WFH – Work From Hotel” Options in Singapore To Check Out

-------------------------------------------------------------------------------------------------------

Not sure whether your company can be qualified for bank loans or alternative lending? Try our A.I assisted loan, and Smart Towkay team will send you a lending report within 24 hours' time. With the lending report, we aggregate and recommend the highest chance of approval be it with BANKS / FINANCIAL INSTITUTIONS or Alternative lenders like Peer to Peer Lenders or even B2B lender!

Got a Question?

WhatsApp Us, Our Friendly Team will get back to you asap :)

Share with us your thoughts by leaving a comment below!

Stay updated with the latest business news and help one another become Smarter Towkays. Subscribe to our Newsletter now!