- 10 Lenders Said No. SmartLend Found the One Who Said Yes — in 3 Days.

- Singapore SME Grants 2023–2026: What Actually Changed (And What Nobody Tells You)

- Why SME Loan Approval Rates Dropped to 70% — And What the Iran War Means for 2026

- Real CBS Makeovers: 3 Case Studies of SME Owners Who Turned Bad Credit Around

- Ask SmartLend: Why Did My SME Loan Get Rejected?

- Introducing SmartLend Concierge: A Helping Hand for SME Loans

- Legal Ways to Lighten Your Company’s Tax Burden in Singapore

- A Wake-Up Call on Director Duties: The Envy Saga and Other Cautionary Tales in Singapore

- Surviving Cash Flow Crunch: How SMEs Can Use Short-Term Financing Wisely

- Unmasking Business Loan Fraud: How Syndicates and Rogue Brokers Game Singapore’s Lending System—and How AI Can Stop Them

Why Worker’s Party MP Jamus Lim Should Stick To His Day Job: Remortgaging When Interest Rates Are Low

So the golden boy of the Worker’s Party did an ‘IP Man’ on his maiden speech in Parliament on 3rd September 2020. Worker’s Party MP Jamus Lim faced heavy artillery as a total of 7 Members of Parliament from the People’s Action Party (PAP) questioned his call for a universal minimum wage policy. A lot of public debates were focused on the minimum wage policy, however, another topic in question is the "Remortgaging" concept that MP Jamus Lim has brought up.

Quoted from Todayonline.com:

Dr Lim advocated otherwise on Thursday, stating that the Government should instead “make the best use of financial resources and not cling to some rigid ideology that we should never touch (the reserves)”.

Instead of over-saving, money can be invested in other needs such as on the youth and education, which would ultimately pay out “higher returns” down the line, the Sengkang MP said.

He likened it to the concept of remortgaging, in which people refinance their home loans to take advantage of the present low-interest rate environment in order to expand their leverage.

This led Potong Pasir MP Sitoh Yih Pin, a chartered accountant by profession, to challenge Dr Lim’s assumption that spending the reserves will definitely generate better returns.

“I can tell you that (remortgaging) is how people start getting into trouble. I hope you're not teaching that in your classes,” Mr Sitoh remarked.

So what is “Remortgaging” or rather, we believe what he meant is Home Equity Term Loan in the local bank’s context. Remortgaging is simply “Refinancing”, which means to re-mortgage your existing property to another bank at a lower interest rate for interest savings.

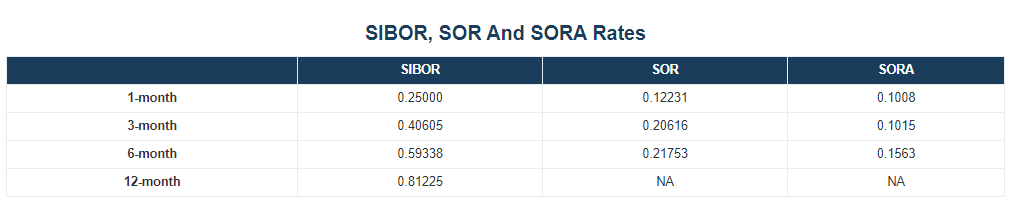

In MP Jamus Lim’s context, he meant to leverage on your existing property to ‘cash out’ and get an equity term loan out of it. Of course, this makes perfect sense given the low interest climate currently as SIBOR & SORA (Singapore Interbank Offer Rate & Singapore Overnight Rate Average) is on a downward trend due to the COVID-19 pandemic.

Example: Say your private property is valued at S$1,000,000. Existing bank loan is S$300,000 with S$200,000 CPF usage. Depending on your TDSR (Total Debt Servicing Ratio) calculation, a home equity term loan capped at 75% of Loan to Valuation (LTV), a homeowner can ‘cash out’ S$250,000 from their property.

As of 10/09/2020, 3-month SIBOR (which is what most home loan packages are pegged to) is at 0.40605% compared to > 1.5% at the beginning of 2020.

But there are alot of factors that determine if one should take out an equity term loan against their property in this current climate:

1. Economy Outlook: The current low interest climate for home loans is due to the United States Federal Reserve (The Fed) slashing interest rates to near zero in recent time. This, of course, has a knock-on effect on Singapore’s interest climate, sending SIBOR rates to as low as the current 0.4%.

This is where MP Jamus Lim’s economics background comes in, as he believes that interest rates will remain low in the near future thus with current home loan mortgage as low as 1.15%, it makes perfect sense to borrow at low (1.15%) and invest in higher yield investment products.

But this is a flawed assumption, as banks will eventually adjust their spread and with the recent announcement to shift from SIBOR-linked home packages to SORA, and interest rates normality will eventually resume. Furthermore, cheap interest rates means that more people will rush in to buy properties, as seen in 2009, which we assume the government will step in if it becomes too attractive.

2. HDB Loan: More than 80% of the Singapore’s population lives in HDBs, however HDB owners are not allowed to borrow against their flat for equity term loan. And EC (Executive Condominium) owners will need to wait till their Minimum Occupation Period is fulfilled for their EC to be privatized. This leaves us with only 20% of Singaporeans who stay in private properties i.e condominiums and landed estate, to be able to utilize this ‘remortgage’ concept.

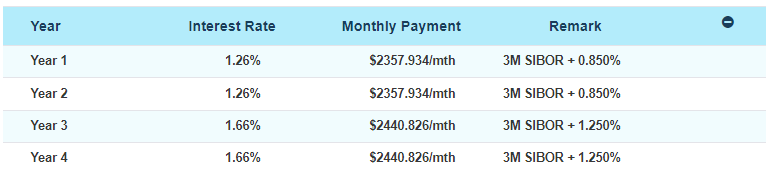

3. Bank’s Home Loan Package: Financial Institutes seldom have a perpetual interest rates package, most offer letter clause will look similar like below:

One may notice that interest rates tend to hike after the 2nd year lock-in period, thus if the equity term loan is used to invest in higher yield investment products, one has to factor in the payment for Year 3 interests in the event that no refinancing is done at lower interest rates then.

If banks further increase their spread, which is 1.25% in the above example in the 3rd year, one might have to find an even higher investment returns to make this worthwhile.

4. Return On Investments (ROI): Bearing in mind that the borrower will still have to repay the monthly installment on the equity term loan. (There’s no interest only package for home loans in the market now)

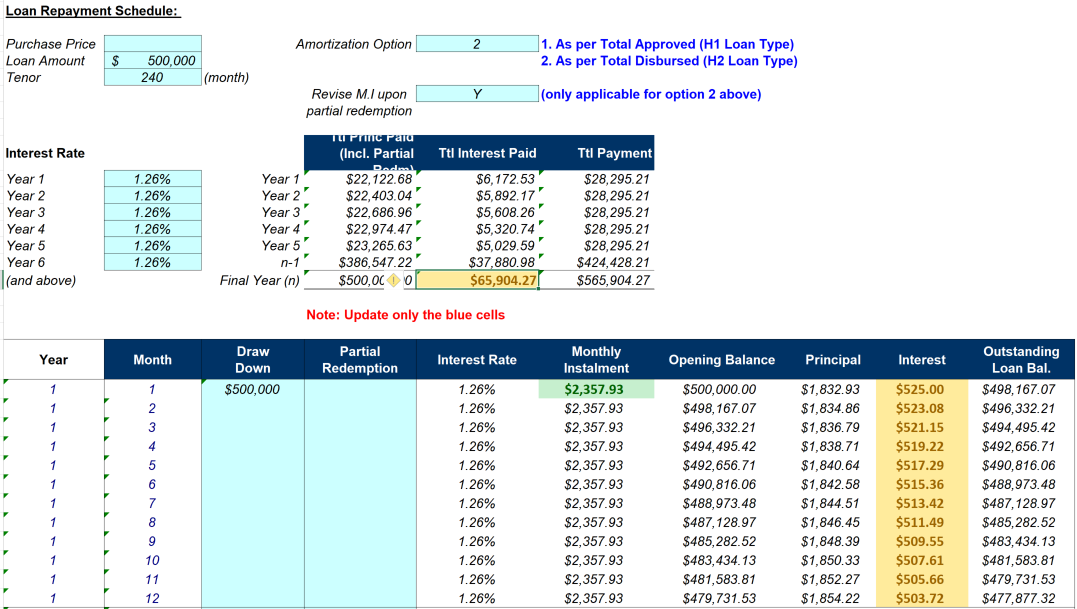

Example: S$500,000 equity term loan of 20 years at 1.26%, one has to pay a monthly installment of S$2,357.93. Annual installment payment works out to be S$28,295.21

As most investment products give returns on a yearly basis, say we manage to find an investment return that yields 3.25% effective (E.I.R) yearly without factoring management or policy fees (if it is an insurance-linked product).

Total interest repayments throughout the whole loan tenure is S$65,904.27 vs Investment Yield of S$165,517.12.

Sounds great? Earning a whooping S$100,000+ for a 20 years tenure.

But bearing in mind that most investment products are paid out on a yearly or in some cases, like bonds, semi-annually.

Your yearly commitment by taking a home equity term loan will be at S$28,295.21 while on average your annual returns from the investment is S$8,275.85. That’s an additional S$20,000 per annum cash-outlay throughout the loan tenure.

The next question you have to ask is, if the additional monthly installment commitment is something that you can afford, and not forgetting the fact that the returns from the investment will only cover your interest expense but not the principal amount.

Okay fair, what about using the “cash out” to purchase another property? (I mean, with all the Youtube videos out there citing low cash upfront and earning good rental returns, etc)

Using Home Equity Term Loan to pay the downpayment of another property has its pros and cons, which have been discussed several times, and we would not be going into details.

But in Summary, TLDR

1. The fact that you have an existing property means that if you want to purchase another residential property, you will incur Additional Buyer Stamp Duty (ABSD).

2. Yes, you could purchase an Industrial/Commercial Property. But unless you have an operating company, given the TDSR guideline, and with the additional commitment due to the “cash out” from the equity term loan factored in, the chances of getting a mortgage loan to finance 80% of the new purchase will be quite slim.

Notwithstanding that Industrial/Commercial Property will incur GST, which is waived for Residential Properties, this adds as an additional cost for you. (Of course, you can set up an investment holding company and voluntarily register for GST.)

Read also: 5 Key Things SMEs Need To Know About Being GST-Registered 2020

3. The Return on Investments (ROI) depends on 3 factors:

- Rental Income (that’s provided there are rental proceeds every month to service the monthly installment throughout the whole tenure)

- Capital Appreciation (Given the current uncertain economy climate, no one can guarantee what will be the increase in valuation)

- Miscellaneous Charges such as MCST, Utilities, Renovation, etc.

4. Total Debt Servicing Ratio (TDSR): So you manage to find an ideal investment product. What’s next? Well, you have to pass the TDSR guidelines from MAS to qualify for the equity term loan.

TDSR: Your monthly debt cannot exceed 60% of your monthly income. Debts include your home loan repayments, credit card bill, car loans, personal loan, etc.

This is also provided that your income will only increase over the years, as any changes to your fixed income will affect your next refinancing, should there be lower interest rates. Your loan will also be subjected to review or clawback if you default on the payments.

What if you failed the TDSR but still keen to take up an equity term loan?

If you are a business owner with an operating private limited company, good news is that there are financial institutions out there where you can pledge your personal property for a equity term loan under a corporate entity. (In this case, no TDSR assessment will be required).

Contact us to find out more if you would like to explore this option.

Read also: Should You Refinance Your Property Loan In 2020?

Conclusion

So is Potong Pasir MP Sitoh Yih Pin, a chartered accountant, right in saying that people are getting into trouble by remortgaging? Yes and No. Leveraging on properties has been a well known concept for years, as it always makes sense to leverage on low interest rates to invest in higher yield products.

At the end of the day, it boils down to the usage of the equity term loan and the investment products. Some may use it as a start-up capital or as additional working capital for their new/existing businesses as home equity term loan is still cheaper than an unsecured business term loan, and it offers a much longer tenure for lower monthly commitment compared to a maximum 5 years tenure for business term loan.

Read also: 3 Ways a Business Loan Can Help To Grow Your Business 2020

Nonetheless, one has to be prudent in choosing their financial products, and take into consideration whether or not they could service the additional monthly installment that arises from this “cash out”. Given the current COVID-19 situation, job security is in everyone's mind, do you want to over-leverage yourself and take the risk of additional monthly commitment?

Another common usage of an equity term loan is to use it as a means to pay off existing personal debts such as personal loan, credit cards, car loans, etc as it makes perfect sense to take the equity term loan from your mortgage to do a full payment on personal liabilities as you are using a lower interest loan to pay off a higher interest debt.

Read also: What You Need To Know About Home Equity Loans 2020

-------------------------------------------------------------------------------------------------------

Not sure whether your company can be qualified for bank loans or alternative lending? Try our A.I assisted loan, and Smart Towkay team will send you a lending report within 24 hours' time. With the lending report, we aggregate and recommend the highest chance of approval be it with BANKS / FINANCIAL INSTITUTIONS or Alternative lenders like Peer to Peer Lenders or even B2B lender!

Got a Question?

WhatsApp Us, Our Friendly Team will get back to you asap :)

Share with us your thoughts by leaving a comment below!

Stay updated with the latest business news and help one another become Smarter Towkays. Subscribe to our Newsletter now!